"in North America, there is no nostalgia for the postwar period"

This was the point in the chapter where I had to stop and boggle for a minute, and it's just as bogglesome the more I think about it. His direct point is about overall growth rates, and how they were so much higher in the postwar decades in Europe, whereas the US had been slightly higher for a long time and didn't get a huge boost. However, the question of nostalgia would seem to be one that is crucially affected by distribution, and many individual Americans certainly did better during this period.

I was wondering if maybe the French are nostalgic for the postwar period in an incredibly more intense way that makes US nostalgia look not worth mentioning to Piketty? The transition from thirty years of war and depression, with the war largely taking place on French soil, to peace, prosperity, and high economic growth had to be pretty intense.

I don't think the British are really that nostalgic for the post-war period. Maybe a bit, but folk-memory is largely of it as a period of austerity. High-growth and prosperity is, in folk-memory at least, more a 60s thing.

My guess is that Piketty's generational averages led him astray - 1913-1950 looked a lot better for the US than for France, but that's because it averages out the Depression.

re: 4

I'm pretty sure 1913-1950 really was quite a lot better for the US than for France.

3: This is entirely based on novels, like everything else I know about the world. But I have a sense of the immediate postwar period in Britain as seeming like a period of austerity precisely because of redistribution -- all the fiction I can think of is formerly rich people lamenting that they can't keep up their estates any more, and that the money they need for the simple necessities of life like servants is being taxed away at ruinous rates to provide the lower classes with frivolous luxuries like false teeth.

I can't think of anything I've read that provides a working-class perspective on the 50s in the UK, but it seems as if that might be brighter.

5: Fewer artillery barrages will do that for a country.

I like his two sentence dismissal of the service sector as a useful classification. In fact brusque clarification through polite dismissal is a technique he seems rather expert at.

I did not realise the extent to which inflation was a twentieth century phenomenon. It always seemed like a fact of life to me. There are some famous historical episodes, such as after the invention of paper money in Song China, the collapse of terms of trade at the end of the Ming (due to Spanish silver mining in South America) or inflation during the American Revolution again due to the issuing of a lot of paper. It seems these are genuine outliers, moments of great upheaval against a background of sound money. The three top of the head examples I came up with also all happened to be "early modern" phenomena too.

It almost gives me moment of sympathy for gold bugs, because that is how money worked for most of history. I was luckily able to quickly squash this. Nutters.

We get the first burst of literary examples at the end of Chapter 2. Reviewers all swoon over these, with exclamations of how well-rounded and French he is, but it's worth noting they are not just colour to make the book accessible to liberal arts educated book reviewers. They are part of his technique as a historian - he is testing the big data stats work for consistency against more qualitative or at least case study evidence from the same period. This is despite his book title following a template from Buck Rogers.

More of 6: That is, there's got to be a generation of people who grew up in "The Road To Wigan Pier", six to a room and with a toilet overflowing with sewage in the back yard, who fought in WW II and came home to decent housing and available work. I can't think of what I've read from that perspective, but those guys must have thought well of the 50s.

Indeed. For four out of the first five years of that period, the French lost a thousand men killed every day. For four of the last ten they were occupied by Nazis. In between they shared the experience of the depression with the US. One out of three ain't bad, I suppose.

6. Food rationing in Britain didn't end until 1954. Austerity was pretty damn austere. Better than the immediate post war years, but still quite hard for everybody. Of course there were benefits, like the NHS, but day to day, not much nostalgia, as ttaM says.

Did you at least get better rations than in 1941?

re: 6

Well, the UK had rationing until 1954. So the post-war years really were a period of genuine hardship for everyone. On the bright side, NHS plus big housebuilding programs, among other things, but those took a while to kick in.

Pwned almost verbatim by Chris Y.

Well, the French call the period 1945 to 1975 les trente glorieuses, the 30 glorious years.

Piketty notes that Britain like the US had relatively steady growth compared to continental Europe. I didn't notice any particular fifties nostalgia when there or in a lifetime of British pop culture consumption, maybe a native would contradict. WWII and sixties nostalgia much more common. NHS-nostalgia pretty widespread. Maybe Piketty was led astray by over generalizing after his time at the LSE.

re: 16

Best in winter, when sometimes you got the wee extruded ice-milk lolly out of the top of the bottle.

I didn't actually make it to the nostalgia line yet, but it brings to mind a trick question on a 10th grade US History quiz that still irks me. The question was basically "How would you describe the economic situation of the US following WWII?" and the answer was "Recession". Because apparently there was a little recession just after the war, for the obvious reason that a whole bunch of tank orders got cancelled. But there was no clarification in the question that we were talking about "1946-1948" or whatever the period in question actually was. So what does "post-war" mean in the Pikettyverse? Obvs. we all know that there was rationing in Britain until Thatcher came to power and purged all the Communists, but I would still think of say, 1960 as being "post-war" in many ways. When does "post-war" end in the US? The Tet Offensive?

Not many people realise this, but the worst rationing was actually post-war. Bread wasn't rationed until 1947 iirc (when we needed the spare grain to prevent a famine in occupied Germany, amazingly). Much of the UK economy was diverted first to war production, and then after 1945 into exports to pay off the US loan (which we finally finished in 2006)

I was speculating that even with food rationing, the mass of the population might have seen a rise in their standard of living from, say, 1937 to 1947. I remember reading that the children of the rationing generation were significantly taller and healthier than than immediately prior generations. But of course it would make sense for rationing to feel like a hardship even to someone who was objectively eating better under rationing than they had been before it was imposed.

5: I agree - I should say it correctly averaged out the Depression for the US - but the Depression was still a huge thing in itself, even if it was bookended by better times, so Piketty misses the cultural impact.

21: What, because of rationing putting a minimum on food consumption and helping those at the bottom? Are you sure it worked that way? In the US, at least, you still had to pay for food; the ration stamps just gave you the right to do so. Though there were also price controls.

I can have a go at he summary for chapter 6 or 7.

21: On that "Supersizers Go WWII" show, they said that vegetables were completely not rationed during the war, and presumably also after. So, not hard to imagine that you grow up taller and stronger if you have to eat carrots instead of bread and dripping or a choco-lolly.

19: In context Piketty is talking about late 1940s to early 1970s. His Figure 2.3 shows that the growth rate in the US was relatively flat from the mid 19th century to now, compared to Europe where 1913-1950 was obviously disastrously low and 1950-1970 very very high. But it almost seems like he's inferring a cultural fact about nostalgia from an economic one, as if he didn't bother to ask anyone what they think. And at least my sense is that Nathan gets it right in 1: this is the growth of per capita output, but tells us nothing about relative effects of growth on different groups, which is where the nostalgia comes in.

re: 21 and 23

Minivet is right, people still had to pay for food.

Unemployment was lower, though, throughout the war and after. By quite a bit. In fact, it didn't really rise again until post-Oil Crisis.

That makes sense. I must've stopped reading just before that part.

I guess maybe the question to ask is precisely what kind of nostalgia do we in the US feel for 1945-1970? Mostly, we grumble a lot about how there was much closer to full employment (for white people) back then, and libraries were fairly well-funded. Certainly most people (who are not Pat Buchanan or Ann Applebaum) are not that nostalgic for HUAC.

I was thinking about this a bit while watching some of Slacker last night, in that the kind of lifestyle depicted for young Austinites in 1989 in the film would be pretty difficult to maintain on a part-time, minimum wage job, or would entail much larger student loans nowadays.

Not to make any point, but apropos, Reconversion Blues is a very fun song.

17, 21. No. No nostalgia at all. Yes, people were probably aware that the basics were more securely available than before, but there were no nice things. Those started in the 60s (the first half, between the end of the Chatterley ban...) Post war to me (b. 1951) ended with the "little recession" in the early 70s.

I concur with conflated's point about the literary examples. That approach really appeals to me.

As far as the nostalgia goes, I also wonder about 2. Also I wonder if nostalgia for that era in France is less tempered or less ideological than it (currently, at least) is in this country?

but the Depression was still a huge thing in itself, even if it was bookended by better times

Yes. Excepting those who got sent overseas, World War II was a prosperous time for my family. The only difficulty anybody talks about is not having tires. Food was rationed, but not very onerously. My dad talks about getting ice cream and cake after dinner every day. Grandpa would trade meat for the sugar rations of older relatives and neighbors who didn't have five kids and a sweet tooth.

Piketty says (on page 98 for those using paper) that UK growth was noticeably lower than in the rest of Western Europe, more similar to North America, and even suggests this as part of the reason for Thatcher.

I think the "nostalgia" thing is definitely wrong w/r/t American liberals as put (don't really know about the UK one way or the other) but I think the point he was trying to make is that there's a very different consensus in the US/UK than France/Germany about the conditions for rapid economic growth.

In France/Germany, you had genuinely massive economic growth combined with a massive expansion of the social state, so the two seem intimately connected. In the US there's a powerful, if largely false, narrative that the period 1950-1980 saw a shackling of the economy/slowdown of growth/loss of national dominance, until saint Reagan restored the possibility of rapid growth again. I know that most people here don't share this view but until very recently even most Democrats would have told you that the overall US economic policy of the 1960s-70s "didn't work" which is why they needed to be replaced by neoliberalism. In other words, a slide or stagnation from a peak in about 1950 to a valley in 1980 or so, and then a purported revival of growth achieved by abandoning the social state. Again, not saying US liberals think this now but it was a pretty common narrative until at least very recently.

France and Germany, on the other hand, look to the whole 1945-75 period as one of unambiguous consistent success; the social state is linked with rapid economic growth. That's the difference.

No idea about the UK, I really don't understand UK politics. I feel like in the 80s-90s there was a lot of stuff about 50s-70s economic policy crippling Britain's international dominance, but maybe that was all Thatcherite propaganda.

Or put more simply there are big differences in elite or quasi-elite conventional understandings of what drives economic growth, due to differing experiences in the 45-75 period.

More interesting to me than the nostalgia line is that Piketty also thinks that the elite discourse in both countries gets it wrong and neither postwar continental social democracy or Reagan/Thatcher liberalization had much of anything to do with economic growth per se (though as he goes on you'll see that he thinks these differences are very very important for distributional equality, just not for growth itself).

19: There was also the recession of 1953, and another in '57-'58. The French at least have a reason for nostalgia for les trente glorieuses; American nostalgia for the '50s is way weirder.

35.2. Yes, I found that the most surprising and interesting part of the argument so far. But only surprising in that nobody had pointed it out to me before.

36: Weren't those pretty short recessions by pre-1940 or post-1980 standards, though?

36: I dunno if it is so much weirder. As above, regardless of the overall economy, there were big changes in wealth distribution internally in the '50s. Pretty much everyone in my extended family did quite well in that period. From hardscrabble farmers to prosperous farmer/workers who took their kids to Disneyland. I don't think that was all that unusual for similarly positioned white people either.

As my English teacher in HS pointed out wrt The Grapes of Wrath -- being a transient Okie was pretty tough, but the next generation would have been growing up during the big, long boom in California, with the best educational system in the country, lots of jobs, etc.

37: Agreed. Maddeningly, commenting from work, I'm working off my memory of the chapter rather than being able to flip through it, but he seemed to be making (without yet really backing up other than by an appeal to the historical record since the beginning of the Industrial Revolution) a claim that growth rates for the countries at the technological cutting edge have been consistently under 2% in the long run regardless of policy, and any higher growth rates have been the result of catching up to that cutting edge.

To the extent this claim is solidly defensible (and that it looks like a reliable prediction about the future), it seems to be a rebuttal to almost all right-wing economic discourse about how policies that tend to increase inequality are justifiable because they lead to higher growth, rising tide lifting all boats, and so on.

Yes, I had exactly the same response to 40.2. I think it's fair to say that essentislly the entire premise of right wing economic discourse was that it promised greater growth (in return for other trade offs). That this premise was basically bullshit from start to finish is something that I've sort of known for a few years, and that Piketty doesn't go into detail over, but it really is a stunning indictment of 30 years of conventional policy wisdom in the US being, basically, total bullshit.

39: As my English teacher in HS pointed out wrt The Grapes of Wrath

A similar thought is how I got through watching The Bicycle Thief without bursting into tears; thinking that five-ten years down the road, Italy was going to be a much, much easier place to live.

With the implication that there will be a slowdown in China, Brasil, India etc. whether or not they adopt different policies in the future; and subsequently in Mexico, Nigeria and the next tranche.

Honestly, if I were a billionaire, I would pay for a huge marble monument in Washington DC that says THERE IS NO EVIDENCE THAT RIGHT WING ECONOMIC POLICY CREATES ECONOMIC GROWTH. With the supporting evidence in a series of stelae on the sides.

re: 44

Or ninja death-squads, to take out any and all 'freshwater' style economists? And all of the CEOs of Fortune 500 companies.*

* plus Ekranoplan, and personal grass-fed buffalo ranch.

There was a whole Nigerian family in McDonald's this morning. Dad, mom, four kids from about 12 through early 20s. I hadn't quite realized before how much Nigerians dress like Nigerians, if that makes sense.

44. Of course, if you were a billionaire you might have rather different views on the subject. But you could try sending a proposal to Soros.

How would you expect Nigerians to dress?

I don't know. The Japanese all dress like white Protestants. The Chinese like not quite so wealthy white people. The various Muslim groups have more or less distinguishing clothing on women, but not men.

I'm kind of imagining the monument topped with a giant statue of Thomas Piketty dressed as an ancient Gaul warrior, raising an axe over the cowering, soon-to-be lifeless corpse of Milton Friedman. Just my personal aesthetic. Maybe not appropriate for the reading group thread.

re: 51.last

Really? I'm used to seeing a lot of guys in either the Somali 'sarong'-like thing, or the low-crotched baggy trousers.

I'm through Part One so far, and it's really hard for me to believe that the completion rate for this book is very high. Piketty is a perfectly good writer, but how many people are going to slog through hundreds of pages analyzing national accounts?

It also seems to early to weigh in on the FT kerfuffle from the end of last week, but Piketty is so clear about measurement problems and how we really can only draw very high-level conclusions from the data that I really don't see how some data issues can actually undermine whatever he is getting at.

Economic growth is the fundamental excuse and rationalization for inequality in today's society. In Chapter 2 Piketty seems to just be saying that growth rates of 3-4 percent -- what many people consider to be "normal" and desirable -- are actually historically very unusual, and as a whole since the Industrial Revolution growth rates of 1-2 percent are much more representative. There's no deep theory here, just a simple consideration of the overall historical record across a number of countries and a couple hundred years.

It's interesting that the power of his argument seems to come from his ability to place the current day in historical context, and in particular his suggestion that the current day does not represent some dramatic break from history. I guess no one really thinks that JP Morgan or Andrew Carnegie were agents for the common good, but it's somehow more plausible to people that raising taxes on hedge fund managers today might cause our economy to grind to a halt.

Piketty is a perfectly good writer, but how many people are going to slog through hundreds of pages analyzing national accounts?

Hence this reading group. I knew I didn't have a shot without some external guilt-trip.

53: I think you may be in a more cosmopolitan area that I am.

Piketty is so clear about measurement problems and how we really can only draw very high-level conclusions from the data that I really don't see how some data issues can actually undermine whatever he is getting at.

This seems to be the emerging consensus: not just people like Krugman and DeLong, but the Economist etc.

The corollary to the proposition that growth rates (in developed countries) aren't terribly responsive to policy decisions is that any change in the relationship between r and g has to be more about reducing r than increasing g.

How much of the book is about data measurement problems? That's far more interesting than economics in general.

"in North America, there is no nostalgia for the postwar period"

It almost seems like Piketty has never watched Happy Days

Slightly more seriously, this strikes me as a naive view of nostalgia --like it requires some basis in the actual reality of how things were.

re: 56

Yeah, I'd guess. I'm in London, and not in a particularly white-British part of it.

How much of the book is about data measurement problems? That's far more interesting than economics in general.

I'm not sure how to quantify it, since it's sprinkled pretty effectively throughout the text. But off the top of my head, in Part One he discusses challenges in measuring inflation, how product and service quality changes over time, how the standard of living varies between countries, what the value of government-provided services is, and what the value of infrequently traded assets is. And he's not running super-fancy econometric techniques to pull a pattern out of the data, he's generally showing bar charts and explaining how the data is really messy but we can still draw some high-level conclusion from the chart -- wealth is 5-6 times income, growth is typically between 1-2% since the industrial revolution, net foreign assets used to have a large share of wealth in France and England but now it's pretty trivial, etc.

but how many people are going to slog through hundreds of pages analyzing national accounts?

It's awfully readable for text about national accounts. What worries me about the reading group is that the handful-of-pages-a-day pace is going to make the book seem a lot longer and more tedious than it actually is.

I'm figuring that people are thinking of it as background reading over the summer. At this pace, no one's focusing on it exclusively, but there'll be enough to talk about it to spend a day or two every week for sixteen weeks.

I don't think the British are really that nostalgic for the post-war period. Maybe a bit, but folk-memory is largely of it as a period of austerity.

What's the Eddie Izzard line about how in the 60s the Americans were working to put a man on moon, and Britain was hard pressed to put a man in a track suit up a ladder . . .

On data measurement problems, I saw a big red flag when he said that the only way to accurately gauge the increase in living standards is "to look at income levels in today's currency and compare these to price levels for the various goods and services available in different periods." But this overlooks the fact that until WWI a huge proportion of the population worked in domestic service, especially women, and a significant part of their remuneration was in kind, board and lodging, cast-off clothes, etc. Isn't there an apples and oranges problem here if you simply look at prices and incomes in earlier periods without accounting for the amount of consumption not formally included in outgoings from income. And how the hell do you measure that if you want to?

Equally, he writes later on, "purchasing power measured in kilos of bread or meat rose less than fourfold, although there was a sharp increase in the quality and variety of products on offer

66.2 continued (dunno what happened there). Yes, they became more nutritious. Don't we need to factor this in somehow? Data measurement problem again, but he doesn't seem to address it.

More nutritious, or more appealing? Not that that changes your larger point, but it seems unlikely that there's more food value to modern bread and meat, on a kilo-for-kilo basis, than there was to bread and meat a hundred and fifty years ago.

Well, food in the first world is less often deliberately adulterated with toxic additives than it used to be; and vermin is seldom sold as meat for human consumption. Nor does beer often contain strychnine any more. That's more nutritious in my book.

Here's a nice reference: "On the adulteration of bread as a cause of rickets", by the same doctor who demonstrated that cholera was a water borne disease.

Yow. I wasn't thinking of that sort of thing, and clearly should have been.

The question in 66-73 is one where I feel like it would be nice to get some input from some real economists. I feel like these are super commonly understood measuring issues but I'm not sure what to say about them and it'd be nice to get some more explanation.

The last time I talked about this stuff seriously was law school, and everything economics related in law school was profoundly unserious. But my impression is that the measurement problem is both well understood and really insoluble in any satisfying way.

By "profoundly unserious" I assume you mean "ideological indoctrination for the guard-dogs of capital."

That was the first time in my life listening to someone and thinking "All my social and interpersonal cues are telling me to approve of this person's politics. And yet when they talk about money, the substance really sounds viciously rightwing." It took me a surprisingly long time to consciously notice the disconnect and start disregarding the "Boy, this person talks like a nice liberal" response I was having to the professors.

But I digress.

When comparing very different societies and periods, we must avoid trying to sum everything up with a single figure, for example "the standard of living in society A is ten times higher than in society B." When growth attains levels such as these, the notion of per capita output is far more abstract than that of population, which at least corresponds to a tangible reality (it is much easier to count people than to count goods and services). Economic development begins with the diversification of ways of life and types of goods and services produced and consumed. It is thus a multidimensional process whose very nature makes it impossible to sum up properly with a single monetary index. P86

I thought he basically caveated heavily and then chose conservative figures. He certainly points out that it depends which goods you are consuming and relies on long term time samples to show up trends. This is the thing that economic data is always a bit of a mess with right ... Lagging indicators, seasonal adjustment, etc. Piketty doesn't need to make seasonal adjustments because it flattens out over forty seasons or more.

I guess someone could argue that he systematically understates growth g vs saving rate r which can probably be better measured.

Also I thought people paid in board would be off the income tax radar before WWI or even later. I would guess an approach would be to say they are still part of the real estate market, price is determined on the margin, therefore they are covered by other property price indicators of price/m2 when determining that part of the cost of living.

I guess someone could argue that he systematically understates growth g vs saving rate r which can probably be better measured.

I think this is my concern. I sort of hoped somebody would explain whether you can do anything about it.

I was thinking about this a bit while watching some of Slacker last night, in that the kind of lifestyle depicted for young Austinites in 1989 in the film would be pretty difficult to maintain on a part-time, minimum wage job, or would entail much larger student loans nowadays.

That's how I felt about Straight Time, a movie of gritty realism from 1978. Dustin Hoffman gets out of jail, treats his parole officer with contempt, goes to the unemployment agency and immediately gets a job at a warehouse or somewhere. And he gets a date with the unemployment agency lady. Then he quits the warehouse job after a day, walks down the street and gets another job. This hopeless situation leads him to enlist his friend (who is actually unlucky, unlike him) into a poorly planned jewelry store robbery, and abduct his parole officer for no apparent reason.

It's a very good movie though. His friend's wife is a young Kathy Bates (practically the only movie to contain a young Kathy Bates).

Anyway, return to your discussion.

66.1 is interesting. I thought Piketty was going to address that when he started talking about nonwage income, but that turned out to be things like farms, restaurants, and other small sole-proprietor businesses where labor income is hard to disaggregate from return on capital.

Similarly, I wonder if he includes the imputed rental value of owner-occupied house in capital incomes.

66: This is probably obvious, but there is no way to straightforwardly compare economic well-being across time. It is surprisingly tricky even to compare economic well-being within a single time period. This is the problem that positing utility/rat orgasms/what-have-you as a summable measure of well-being is intended to address. Income is only meaningful insofar as it tells you something about the person's actual set of consumption choices. That is a very tricky step to take, even if you could somehow equalize 'real' income (and measuring inflation has lots of utility-based assumptions about substitution in it). So you're always dealing with a set of highly imperfect assumptions, it's just important to be clear about what they are. I'm way behind others in reading this book so haven't come to his discussion of how exactly he does that.

A really interesting strain of research to me is studies that take some clear physically measurable output and examine how it changes over time, and how this relates to income-based measures. The most famous examples use anthropometric changes in well-being or health like height. This is convincingly telling you something important, but even if height improves that is not an income measure; society could get richer in many ways that don't directly impact e.g. childhood nutrition. Another interesting example compared changes in output as measured by income to changes in output measured by the cost of generating one unit of light, which is more consistently traceable over time. Here is that paper .

Sorry, the paper compares changes in price levels as measured by price indexes to changes in price levels as measured by the 'true price of light', as measured using physical light output from various technologies. Implicitly that compares output measures based on estimates of real income to a physical efficiency output measure. Obviously you could do this for other physical processes like transportation, heat, etc.

I just finished chapter 2 at lunch and there are still parts of chapter 1 I read while dozing off (not his fault!) that may have covered this, but I was really struck by the part on page 88 where he talks about how many carrots the average earner could buy per day, from 10 kilos to now 60 kilos. And I'm sure this is some normal way of measuring things, but does this mean that all the worker's take-home pay would go to carrots or all the food budget or there's enough left over at the end of the day to buy this many carrots and I'm assuming there are no bulk discounts, right? I just found that part, while not essential to his arguments at all, almost unhelpfully abstract even though it's supposed to be concrete.

Cross-posted with PGD, not ignoring that he has the answers.

I'm pretty sure that's well above the number of carrots required to turn somebody orange.

51: but not men.

Au contraire, there is a very specific style of western dress, or combo western/traditional dress that Somali men tend to affect, at least here in MPLS. I'd say it consists of:

*Baggy dress trousers or khakhis

*Sandals or loafers

*Loose dress shirt, worn tails out

*Keffiyah or skull cap

Plus the dyed-red beards and walking sticks for the older fellows.

You do also see a fair amount of Somali men, young and old, wearing the more traditional thobe/gallebaya/whatever, plus keffiyeh or skull cap, especially if they're going to or from the mosque.

Bringing this back to Piketty, is he going to talk about significant economic disruption as an ongoing feature of global economies at some point? Look at Somalia -- can it even be said to have a national income independent of remittance payments at this point? Or the DRC, where his points from chapter 1 about how prices in less-developed countries are half of what they are in the North/West certainly doesn't apply to things like gasoline, which goes for about $10/liter, I've heard. 60% of the world's weaponry originates in the US -- so the wars that are being fought at any given time are simultaneously destroying wealth in the hinterlands and creating it at the heart of empire.

all the worker's take-home pay would go to carrots

That's how I read it, that a worker's pay was presented in units of carrots rather than money.

I have nothing informed to add to the cost-of-living/basket of goods discussion. But I think that, as P says, the idea of comparing typical goods across many generations is pretty abstract, to the point of being unrealistic.

I'd go farther, and ask if comparing very dissimilar people in the same society makes much sense-- "rent" in a rural county with high unemployment and empty buildings and "rent" in Manhattan are pretty different.

83. That looks very interesting, and I'll have a read. But there must be cases where it's effectively impossible to measure price changes in the face of complete transformations in technology. How do you compare the price of horse tack to car parts, in terms of the cost of maintaining a personal means of transport? Or if you're trying to make it work at a coarser granularity, what is the sum of the inputs that enables getting from A to B on horseback or in a cart that you would need to compare to an equivalent sum of inputs that represents the cost of driving?

One thing worth mentioning is that I'm not sure that the basket of goods issue is particularly important to Piketty's overall point. Unless there's something systematic about the error in measuring growth that would lead to radically upwardly revise growth estimates for the future, or to upwardly revise growth rates for the past such that you could argue that r in fact was less than g for the nineteenth century and before (seems unlikely) an upward revision/nuancing of "g" might matter for historical accuracy and in absolute terms, but wouldn't really affect the overall argument.

Could be wrong about the above.

My in-laws definitely are nostalgic for the post-war period, though possibly only because that was their childhood and people are often nostalgic about their childhood. But I hear a lot about rationing and how sweets tasted better because they had them so rarely and they were healthier, etc, etc. There is a certain romanticism of the deprivation, though not of the cold.

81.2: Pretty sure I remember him making that exact point somewhere in chapters 1 or 2. IOW, yes, he is aware of that issue.

I did not realize the extent to which inflation was a twentieth century phenomenon.

Au contrair. There were also quite significant periods of inflation in the West during the thirteenth, sixteenth, and late eighteenth centuries. The Enlightenment and Victorian era represent fairly stable periods for prices - and those are largely encompassed by Picketty's data. But it has not always been so.

There were also quite significant periods of inflation in the West during the thirteenth, sixteenth, and late eighteenth centuries.

They were however comparatively brief periods, all well short of a hundred years, and in all cases stability subsequently returned. The modern assumption, which is, I think, what Piketty is arguing against, is that the present inflationary period should be assumed to be effectively permanent.

They were however comparatively brief periods, all well short of a hundred years

The 18th century one was fairly brief, but the 16th century one was basically 1492-1648. Turns out that looting a continent has inflationary effects.

OK, I've usually seen that represented as two distinct but close periods. I haven't read Fischer (or heard of him until now), but he may have a good argument for making it a single inflation.

To Alex in 20: I was recently reading somewhere about work on postwar rationing. Apparently the view now is that bread was rationed for political reasons rather than practical ones. Britain instituted rationing at home in order to get the U.S. and Canada to take over responsibility for feeding the population in the British zone in Germany - which made some sense as they were the big grain exporters. The ration was set quite high, basically at pre-war consumption levels, but there was a useful psychological effect, as well as the political one. (Attempting to look it up, I believe the piece I read was from Ina Zweiniger-Bargielowska.)

By the way, I should thank the relevant parties for suggesting and then following through on this reading group. I happened to be reading Piketty on my own, so it was fortuitous for me. I am mostly a lurker, but I'm grateful for the response I've gotten on my few ventures into commentary. So thanks!

One thing I've been wondering about is how Piketty's rate of growth for the US reconciles with historical returns from the stock market that I remembered from my finance courses. From Principles of Corporate Finance (1981 edition), Brealey & Meyers, Table 7-1, the average annual real rates of returns of various US asset classes, 1926-77: Common Stocks 8.7%, Corporate bonds 1.8%, Government bonds 1.1%, Treasury bills, 0.2%.*

Now Piketty is citing per-capita growth rates in Table 2-5, so his figures would be roughly doubled when looking at overall growth, but I'm trying to visualize if these data are consistent with his per-capita growth rates of 1.4-1.9% from 1913-1970 for North America. (Also of course, the former set of figures contribute to r, while he is talking about g in Table 2-5.) And stock market returns tend to be higher to reflect increased risk vs. bonds. But stock market return is ultimately tied to profits, which are tied to output, so I don't know if you can sustain long-term growth rates of stocks that are massively higher than g.

*They cite as their source R.G. Ibbotson and R. A. Sinquefield, Stocks, Bonds, Bills, and Inflation: The Past (1926-1976) and the Future (1977-2000), Financial Analysts Research Foundation, Charlottesville VA 1977, exhibit 38, p. 57, plus unpublished tables for 1977 data.

98: I thought Piketty's whole argument was that economy-wide g could be divergent from return to capital (of which growth in stock prices is a category) r.

99: Yeah, in the limiting case where output and profits weren't growing at all, you would expect stock prices to decline until stocks were basically yielding r + risk premium from the steady state profits. And I would expect most of the benefits of g to go to stocks rather than bonds. So maybe the actual limit on stock market returns is something like r + g + risk premium. In which case, an annual return of 8.7% on stocks might be perfectly consistent with a per-capita growth rate of 1.4-1.9%.

Over the long term presumably the return to capital can't exceed growth, but it can certainly exceed it for long stretches before getting catastrophically reset.

I think both 100 and 101 are wrong!

Yay for calico! Is your name in honor of fabric or cats or something else?

I haven't read Fischer (or heard of him until now)

And yet a bunch of us have recommended Albion's Seed. *sniff*

the average annual real rates of returns of various US asset classes, 1926-77: Common Stocks 8.7%, Corporate bonds 1.8%, Government bonds 1.1%, Treasury bills, 0.2%.*

That's something I've wondered about. I don't know Piketty's explanation, but it seems like an important question. Personally*, I tend to separate the various bonds from stocks and real estate because the former don't (generally speaking) offer opportunities for capital gains. Of the latter, real estate is far from a liquid market and my sense is that until the 70s, there were significant barriers to entry in the stock market, that it was difficult to invest as a retail investor and, for that reason the stock market was consistently undervalued.

I've always assumed that the development of cheap mutual funds (and, less importantly, cheap online brokerages), along with the switch to 401K plans brought a bunch of money into the stock market leading to a one-time inflation in value and reduction in returns.

I would think that as markets become more transparent and more frictionless the rate or return will drop but, again, I don't know if that's the "official" story.

* I don't know how the professionals compare asset classes. Actually, it's too bad that po-mo polymath isn't around for this reading group.

103: Name in honor of the cat. I had one growing up.

Over the long term presumably the return to capital can't exceed growth, but it can certainly exceed it for long stretches before getting catastrophically reset.

I think both 100 and 101 are wrong!

The advantages of a reading group -- I would have had the same intuition as Eggplant but Halford's correct that the book makes clear that is wrong. Let me try to pencil out the

Consider a model in which 80% of productivity growth goes to capital, and 20% goes to labor. If population isn't increasing (to eliminate one variable), productivity grows at 1%/year, and at time T=0, output = 100, and capital stock = 600 (and income to capital = 30)

at T=1 output = 101, income to capital = 30.8

at T=2 output = 102.01, income to capital = 31.608

at t = 10 output = 110.46, income to capital = 38.37

So what's the return to capital? We need to know the total capital stock. If the stock remains at 600 then average return is now 6.45%, but that's unlikely. The rate of return would be 5% if the total capital stock was 767 (which would imply capital accumulation of 16.7/year or ~50% of the income to capital).

If 90% of the income to capital was added to the capital stock then the total would be approximately 900, and the return to capital would have fallen to 4.3%.

So, the return to capital can remain significantly above the growth rate if the return isn't reinvested but (I think), if it is re-invested the rate will approach the rate of production growth.

I think the high return on US stocks since the Great Depression is something of a historical aberration, when you compare to other stock markets and other time periods. It's something of an economic puzzle since the rationalization for consistently higher returns is generally higher risk, but of course consistently higher returns aren't actually that risky. As far as I know there is no particularly clear explanation for it.

107: Fair enough, I was thinking of the return to capital minus the amount consumed.

If anyone wants to play with US stock, bond, and consumption data, Shiller has a spreadsheet here.

Returns on stock have been much higher than the growth rate of the economy. The explanation on why stock retuns have been so high is considered a mystery, known as the "equity premium puzzle."

Though I don't think that's what Piketty means by r. (This confused me too.) For stocks, his r would be the dividend yield. It's a return-on-assets type measure. Income in the national accounts usually doesn't include price appreciation.

He was explicit somewhere that r is anything that could be described as income derived from capital. If you have capital, and then next year you have more capital, and you didn't have income from labor, then the entire ΔCapital, however denominated, is r.

He definitely includes stuff beyond dividends or interest, but I think his income numbers include only realized capital gains rather than unrealized ones. On the other hand, best I can tell his wealth figures include unrealized capital gains.

Where does he say that? On page 54, for example, he says that a property bubble would lower the return on real estate, not raise it.

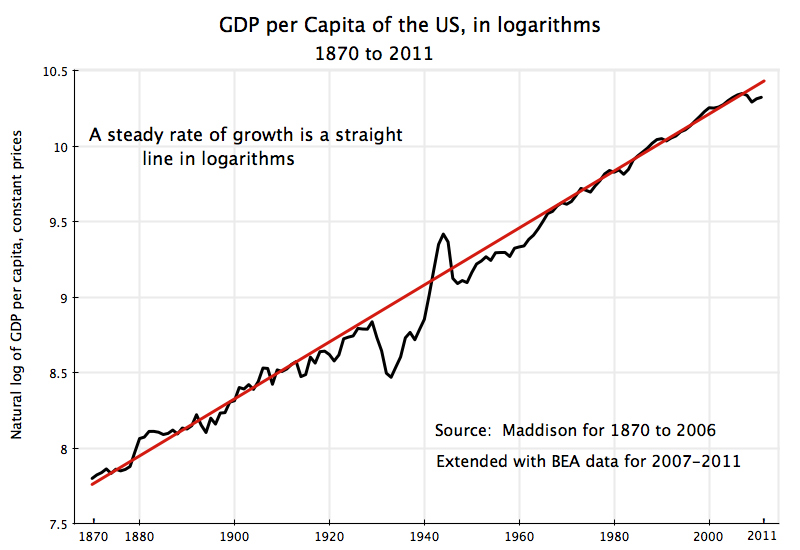

Here is a graph of per capita US growth graphed as a logarithm:

It is very close to 1.9% a year. It even bounces back to the same line after the depression.

I don't have the book here -- I'll look when I get home.

But saying that a property bubble would lower the return on real estate could mean that it would lower the return on real estate after the bubble had inflated. That is, if your real estate is worth X and you receive rents of Y, and a real estate bubble doubles the value of the real estate over the course of a year without changing the rents, you'd have a 100% (+Y) return in the year in which the bubble was inflating, but in all subsequent years your unchanged rent (in absolute terms) would represent half the return (in percentage terms) on the new value of your real estate.

Is that maybe compatible with what you're looking at on p. 54?

"The 18th century one was fairly brief, but the 16th century one was basically 1492-1648. Turns out that looting a continent has inflationary effects."

If you tie your currency to the value of gold and silver, that's what happens when you find a lot of new gold and silver.

112 is my understanding. Unrealized gains not included in r. Realized capital gains from the stock market turn out maybe surprisingly to not be all that super important.

The whole article is pretty good and mentions piketty:

I took this chapter to be saying "Let's establish that the tide rises at 1-2% for all eternity. We're not yet talking about the boats." Did I miss much?

Except that "All eternity" means "Since 1700 or so, but not before that" and "Maybe not in the future, who knows, this is observed history not a law of nature" and "Growth. What's growth? Hard to measure, isn't it."

But generally, yeah.

Ok great. I'm hanging in there for another week, then.

113 On pages 48-49 he implicitly says it when he defines wealth as the sum total of all non-financial assets and financial assets minus debt. He then quickly notes the issue of price volatility, promising to go back to it later on. On page 52 he speaks of the 'rate of return on capital ... regardless of its legal form (profits, rents, dividends, interest, royalties, capital gains, etc)

93: Ah, that is what I would have expected. I misread his graphs - almost every other graph in this chapter runs from antiquity. Though I wonder if some of them to be smoothed out by sparse data.

Head of central bank denounces bankers for increasing inequalty. Should be relevant to the discussion, but not sure how.

He talks about the price of stocks vs other asset classes later, but I am feeling thick and can't quite figure out whether he is saying that the equity premium puzzle is caused by the accounting effect of price increases caused by firms retaining earnings.

If one were to ignore this second component of savings and consider only household savings strictly defined, one would conclude that savings flows in all countries are clearly insufficient to account for the growth of private wealth, which one would then explain largely in terms of a structural increase in the relative price of assets, especially shares of stock. Such a conclusion would be correct in accounting terms but artificial in economic terms: it is true that stock prices tend to rise more quickly than consumption prices over the long run, but the reason for this is essentially that retained earnings allow firms to increase their size and capital (so that we are looking at a volume effect rather than a price effect). If retained earnings are included in private savings, however, the price effect largely disappears.p176

... or whether he is saying that is why he made his statistical choices, and from a point of view of capital stock and savings flows it doesn't much matter to whether you retain wealth as Intel stock or as farmland, the effect is the same. I think the latter.

105: Retail broking is a post-WWII business, they took chain stores as a model. People became more familiar with securities after buying war bonds. Previously there was also much lighter regulation, front running etc was legal. I guess it might have taken a few decades for all of this to wash through the system.

There is already a mountain of Piketty commentary, much more in months than there was for years after Keynes, and I am sadly reading quite a lot of it. I will just link to this one, post one of a symposium at Jacobin, for its erudition, pertinence, and breadth of analysis.

Mentions Hicks 1932 on Marginal Productivity;Marshall, Pareto, Robertson, Sraffa; Cambridge Capital Controversy and Samuelson versus Robinson;etc; and Shamus Khan's ethnography of St Paul's boarding school. Also recommends an important new book on the Aggregate Production Function that should shatter mainstream economics as much as Piketty, or as much as it should have been shattered decades ago.

I have been wondering if I should explain why I have not been participating. Lots of reasons

1) Read Piketty a month ago, pretty sure it is not worth re-reading again so soon.

2) Not sure however good it is, how important the book is. If, as Ackerman explains above, K21 reaffirms that economics is really a function of history, power, class struggle, then will a technical mainstream moderate liberal critique of capitalism have really decisive political effect

3) Moved on to Karatani Kojin and an analysis of capitalism as an exchange economy rather than production economy. Mauss, Wittfogel, Wallerstein.

Reciprocity/tribalism => paternalism/nation => capitalism/democracy => reciprocity/nomadism about to come. Sumpin like that.

4) Inarticulate and born disputatious and tendentious

5) Let y'all do your thing in your own way. I'd most likely just link and cite from the literature anyway.

Huh. Been googling around and can't find any response at all to the Felipe-McCombie work. Somebody called Temple, refuted at Levy.

Lars P Syll discusses Piketty, the CCC, and the comments mention F-M APF. Comments for you:

Felipe and McCombie have gathered all of the compelling arguments denying the existence of aggregate production functions and showing that econometric estimates based on these fail to measure what they purport to quantify: they are artefacts. Their critique, which ought to be read by any economist doing empirical work, is destructive of nearly all that is important to mainstream economics: NAIRU and potential output measures, measures of wage elasticities, of output elasticities and of total factor productivity growth.'

- Marc Lavoie, University of Ottawa, Canada

To my knowledge this has not been successully challenged by the orthodox crowd , so why aren't people like you relentlessly beating them about the head about this ?

It seems like it should be a big deal to me......

Comment by Marko-- 6 April, 2014 #

Yes, McCombie and Felipe's criticisms are damning. Personally, I don't think that the profession could ever take them seriously. Imagine admitting that decades of "empirical" work were based on regressing an accounting identity! Haha! Too funny!

Comment by pilkingtonphil-- 7 April, 2014 #

It might be hard to get an admission from the majority of economists , but I'd view it as tremendously encouraging if , one by one , prominent economists said " Yes , I admit , I fell for this scam , but no more - from now on , reality rules! " Krugman , Stiglitz , Baker etc. could start the ball rolling. As with climate change denial, the last holdouts will look the most idiotic , and those will be the very thought-leaders of the economic paradigm we're trying to displace. ...Marko

{kind=link}